How much you should put down to purchase your new home?

by Pamela Doran

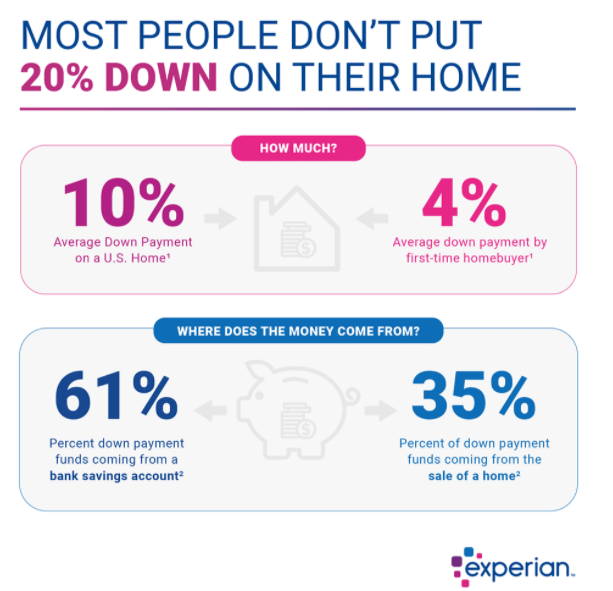

Historically, home buyers seek to put down 20% when they purchase a home.

However, according to a recent survey by The National Association of Realtors (NAR), the actual national average is much closer to 10%.

When it comes to first-time homebuyers, the average down payment is at 4% as per the same survey.

While down payment requirements vary based on the lender you choose to work with, the amount required will usually depend on your credit score and your debt-to-income ratio. On average, most traditional loans require at least 5% down on a new home.

If you’re in a situation when you don’t have a lot of cash, you do have some options. Federal Housing Administration (FHA) loans are more lenient about tough credit (even a FICO Score of 520 can get you an FHA loan) and require as little as 3.5% of the home's value as a down payment.

All of this said, the ideal down payment depends on the price at which you buy your home and your overall homeownership goals. And, rather, than shooting in the dark at an unknown target, you should talk to a lender before you set foot in the door of any home you might consider.

A good lender can help you understand which loan program, and its associated down payment program, would work best for you and your financial situation. There is no perfect number since every situation is unique, especially in light of the large variety of loan programs available in the market today.

Now, if you can save 20% to put down on a home, then absolutely do it. It puts you in the best position to get a great monthly payment on your mortgage. Plus, you get to avoid Private Mortgage Insurance (PMI) on your mortgage. The amount is charged monthly by the lender to ensure that the money gets paid back to the guarantor in the event you default on your mortgage.

Plus, conventional wisdom says that if you have to borrow money - from a friend, family member, your retirement, etc. - for your entire down payment, then you probably shouldn’t be buying a home. The reason is that there are many expenses that you’ll incur above and beyond your mortgage to own your home. In addition to normal utilities and upkeep on your house, there are things like roof leaks, hot water heaters that die, furnaces that don’t heat and other things that will take additional money on your part.

In certain instance, you don’t have the money to buy the home, then you don’t have the money to own the home. It’s a good rule of thumb.

Where does down payment money come from?

Not surprisingly, 61% of home down payment funds come from a bank savings account, and another 35% comes from the sale of another home. The remaining 4% most often come from cash gifts from family or friends.

Cut Spending

If you’re looking to save money for a downpayment, one thing you can do is to identify where you are spending money unnecessarily and limit or cut that spending. It’s key that you know exactly what’s happening with every penny in your budget before you make a huge commitment to buy a home. In many cases, people are spending money they don’t realize they could be saving either for a downpayment or to take care of their new home after they move in.

Early Deduction

One of the best ways to save money for a downpayment is to have money deducted automatically from your paycheck at each pay interval. By “paying yourself first”, you guarantee that you put away the money you need for a downpayment. In addition to that, if you don’t see it before it comes out, then you’ll be less likely to spend it later on. If you feel the need to add a higher layer of protection from spending the money, put it in low-risk investment vehicle that has penalties for early removal (or that prevents early removal period).

Find the best mortgage for you

Being able to come up with the requisite amount of money for your down payment might be as simple as finding a great deal on a home loan. Getting the best loan for your needs will determine how much you need to put down. You might be able to get access to a low-down-payment, and even a no-down-payment, loan that works great for you and your financial situation. With so many loan programs out there, it’s highly possible you’ll find a program with a down payment and monthly mortgage payment that suits you perfectly.

Currently, there are at least six government-backed loan programs today that require 5% down or less:

-

U.S. Federal Housing Administration Loan

-

U.S. Veterans Administration loan

-

Fannie Mae HomeReady loan

-

Fannie Mae Conventional 97 loan

-

A conventional mortgage loan

-

U.S. Department of Agriculture loan

Plus, there are roughly 2,300 down payment assistance and grant programs out there that make interest-free and/or non-recourse loans to qualified home buyers looking for funds.

Once you've determined how much money you need for a home down payment and have a plan to save what you need, you’re now on the path to owning your own home.

As you’re putting your saving plan into action, make sure you take into consideration the additional home purchase costs you’ll likely incur like home inspections, appraisals, moving your family, etc. These expenses can can add thousands of dollars when you sign your home mortgage. A good lender will be able to identify exactly what these costs will be and how much you’ll need to cover them.

The most important thing is to have a plan and do what you need to do, everyday, to save the money you need so you can put it down on the purchase of your new home.